The smart Trick of Paul B Insurance That Nobody is Discussing

With residence insurance, for instance, you can have a substitute cost or actual cash money value plan. You should always ask exactly how cases are paid and what the claims procedure will certainly be.

They will tape your claim and also explore it to discover what happened and also how you are covered. Once they determine you have a covered loss, they may send out a check for your loss to you or maybe to the repair work store if you had an automobile crash. The check will be for your loss, minus your insurance deductible.

The thought is that the cash paid in insurance claims over time will certainly be less than the complete costs collected. You may seem like you're tossing money gone if you never ever file a case, yet having piece of mind that you're covered in the occasion that you do endure a considerable loss, can be worth its weight in gold.

Some Known Details About Paul B Insurance

Visualize you pay $500 a year to insure your $200,000 house. You have 10 years of paying, and also you have actually made no claims. That appears to $500 times ten years. This indicates you've paid $5,000 for house insurance coverage. You begin to question why you are paying so a lot for nothing.

Because insurance is based on spreading the risk amongst many individuals, it is the pooled money of all people paying for it that enables the firm to build properties and cover insurance claims when they occur. Insurance coverage is a company. It would be nice for the firms to simply leave rates at the same degree all the time, the truth is that they have to make sufficient money to cover all the possible insurance claims their insurance holders might make.

just how much they got in premiums, they need to revise their prices to earn money. Underwriting adjustments as well as rate rises or reductions are based on outcomes the insurance coverage firm had in past years. Relying on what business you acquire it from, you may be managing a captive representative. They sell insurance policy from just one business.

Some Known Questions About Paul B Insurance.

The frontline individuals you deal with when you purchase your insurance are the agents and brokers who represent the insurance company. They an acquainted with that firm's items or offerings, yet can not talk in the direction of various other firms' plans, pricing, or product offerings.

How much threat or loss of money can you assume on your very own? Do you have the money to cover your prices or financial obligations if you have a crash? Do you have special demands in your life that need extra protection?

The insurance coverage you need differs based upon where you go to in your life, what kind of properties you have, as well as what your long term objectives and obligations are. That's why it is essential to take the time to discuss what you desire out of your policy with your representative.

Paul B Insurance Fundamentals Explained

If you get a loan to get a car, and then something takes place to the vehicle, void insurance coverage will certainly repay any type of section of your car loan that typical auto insurance policy does not cover. Some lending institutions require their debtors to lug gap insurance policy.

The primary purpose of life insurance policy is to provide money for your beneficiaries when you die. How you pass away can identify whether the insurance provider pays out the death advantage. Depending upon the sort of policy you have, life insurance policy can cover: Natural fatalities. Passing away from a cardiovascular disease, disease or aging are examples of natural deaths.

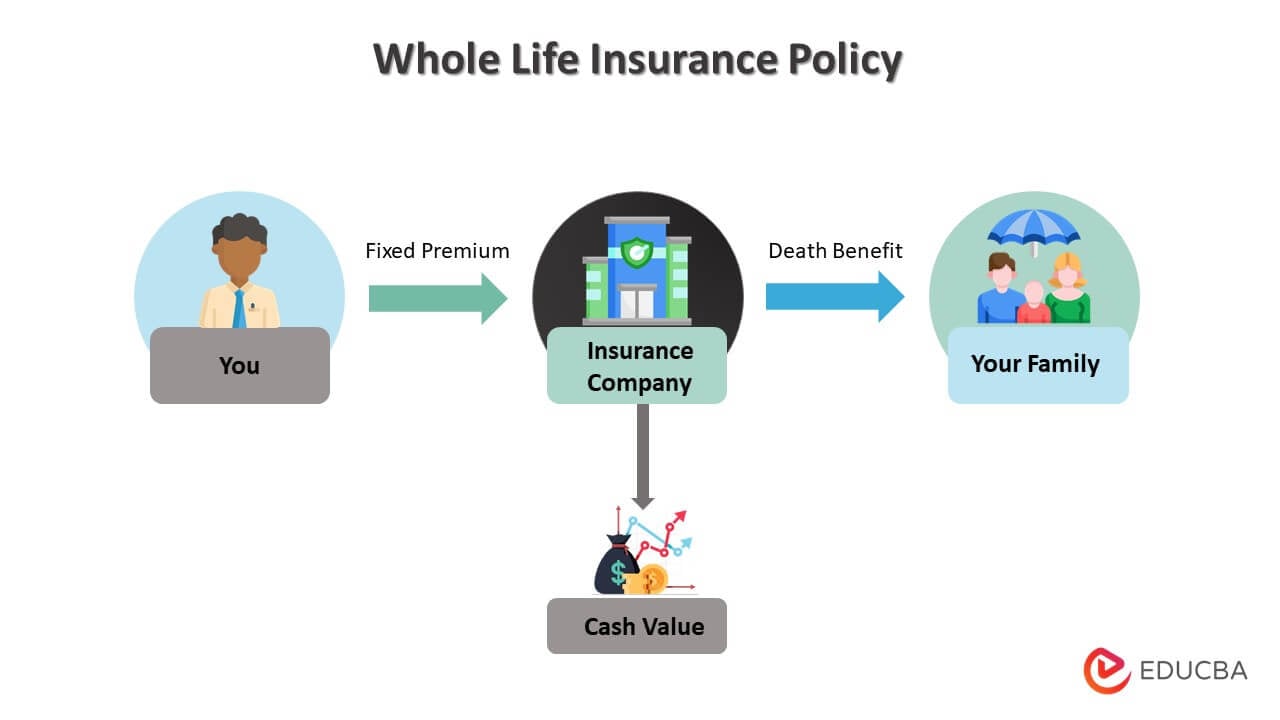

Life insurance policy covers the life of the guaranteed person. The insurance holder, who can be a various person or entity from the insured, pays costs to an insurance provider. In return, the insurance firm pays a sum of cash to the recipients noted on the plan. Term life insurance policy covers you for a period of time chosen at acquisition, such as 10, 20 or thirty years.

About Paul B Insurance

If you don't die throughout that time, no one makes money. Term life is popular since it supplies large payments at a reduced cost than long-term life. It also supplies coverage for a set variety of years. There are some variants of common term life insurance coverage policies. Convertible plans enable you to transform them to permanent life plans at a greater costs, permitting longer and also possibly much more versatile insurance coverage.

Long-term life insurance policy policies build cash value as they age. A portion of the premium repayments is added to the money value, which can make rate of find out interest. The money value of whole life insurance coverage policies grows at a fixed rate, while the click here for info cash value within global plans can rise and fall. Visit Your URL You can make use of the cash money worth of your life insurance policy while you're still active.

If you contrast ordinary life insurance policy prices, you can see the difference. $500,000 of whole life coverage for a healthy 30-year-old female expenses around $4,015 every year, on average. That same level of coverage with a 20-year term life policy would set you back approximately about $188 yearly, according to Quotacy, a broker agent firm.

The Buzz on Paul B Insurance

Variable life is one more irreversible life insurance alternative. It's an alternative to entire life with a fixed payment.

Right here are some life insurance policy basics to help you much better recognize how protection works. For term life policies, these cover the expense of your insurance policy and administrative prices.